This article reproduces the out-of-sample analysis of Welch and Goyal

(2008, RFS) for the log dividend-price ratio

as a predictor of the annual log equity premium. The bundled

wg2008 dataset is built from WG’s original

PredictorData.xls (annual sheet), the data vintage shipped

with the published paper. The effective sample is 1872-2005 (134

annual observations), matching WG: the file itself begins in

1871, but the one-year lag in the predictor consumes that first row.

The benchmark is the prevailing historical mean (NULL). The alternative is a predictive regression on the lagged predictor (ALTERNATIVE). The predictor is

per WG Section 1, where

is the 12-month moving sum of dividends and

is the S&P 500 price level. (The public plotting script

goyal-welch-plots.R uses the level D/P, but WG’s paper text

and Table 1 use the log form.)

WG report five OOS statistics per predictor in Table 1, all of which we compute on the same data:

- : out-of-sample (Campbell-Thompson 2008).

- : .

- MSE-F: McCracken (2007)

-statistic

for equal MSE (

mse_f_test()). - ENC-NEW: Clark-McCracken (2001) encompassing test

(

enc_new()). - CW MSFE-adj: Clark-West (2007) MSFE-adjusted

-statistic

(

cw_test()), which WG report in footnote 2.

library(forecastdom)

library(ggplot2)

data(wg2008)

# WG (2008) Table 1 covers 1872-2005, the entire bundled file.

wg <- wg2008

c(first_year = min(wg$year), last_year = max(wg$year), n = nrow(wg))

#> first_year last_year n

#> 1872 2005 134Helper: recursive forecasts (WG procedure)

The recursive setup matches WG’s goyal-welch-plots.R

exactly:

- At each year

t, refitlm(logeqp ~ log_dp_lag)on years 1…t-1. - ALTERNATIVE forecast for year t = fitted value at the

contemporaneous

log_dp_lag[t]. - NULL forecast = mean of

logeqpover years 1…t-1.

recursive_forecasts <- function(y, x, R) {

n <- length(y)

P <- n - R

e_N <- e_A <- f_N <- f_A <- numeric(P)

for (j in seq_len(P)) {

idx <- seq_len(R + j - 1)

f_N[j] <- mean(y[idx])

fit <- lm.fit(cbind(1, x[idx]), y[idx])

f_A[j] <- sum(coef(fit) * c(1, x[R + j]))

e_N[j] <- y[R + j] - f_N[j]

e_A[j] <- y[R + j] - f_A[j]

}

list(e_N = e_N, e_A = e_A, f_N = f_N, f_A = f_A, year = wg$year[(R + 1):n])

}Table 1: five tests across three OOS specifications

WG explore three OOS-start dates: 20 years after the data begins (around 1892), 1965, and the most recent 30 years (1976-2005). The reported is the adjusted out-of-sample that WG quote in Table 1, applied to the OOS sample of size :

with parameters (intercept plus predictor).

specs <- list(

list(label = "1892+", R = 20L),

list(label = "1965+", R = which(wg$year == 1964)),

list(label = "1976+", R = which(wg$year == 1975))

)

run_spec <- function(spec) {

fc <- recursive_forecasts(wg$logeqp, wg$log_dp_lag, R = spec$R)

MSE_N <- mean(fc$e_N ^ 2)

MSE_A <- mean(fc$e_A ^ 2)

T_oos <- length(fc$e_N)

R2 <- 1 - MSE_A / MSE_N

R2bar <- 1 - (1 - R2) * (T_oos - 1) / (T_oos - 2)

dRMSE <- sqrt(MSE_N) - sqrt(MSE_A)

msef <- mse_f_test(fc$e_N, fc$e_A)

enc <- enc_new(fc$e_N, fc$e_A)

cw <- cw_test(fc$e_N, fc$e_A, fc$f_N, fc$f_A)

data.frame(spec = spec$label,

T_oos = T_oos,

R2bar_pct = 100 * R2bar,

dRMSE_pct = 100 * dRMSE,

MSE_F = unname(msef$statistic),

ENC_NEW = unname(enc$statistic),

CW_stat = unname(cw$statistic),

CW_p = unname(cw$pvalue))

}

tab <- do.call(rbind, lapply(specs, run_spec))

knitr::kable(

tab, digits = 3, row.names = FALSE, format = "html",

table.attr = "style='width:auto;'", escape = FALSE,

caption = "\\(\\bar R^2_{OS}\\) and \\(\\Delta\\mathrm{RMSE}\\) in percent.",

col.names = c("Spec", "\\(T\\)", "\\(\\bar R^2_{OS}\\)",

"\\(\\Delta\\mathrm{RMSE}\\)",

"MSE-F", "ENC-NEW", "CW stat", "\\(p\\)-value"))| Spec | MSE-F | ENC-NEW | CW stat | -value | |||

|---|---|---|---|---|---|---|---|

| 1892+ | 114 | -2.061 | -0.107 | -1.305 | 0.479 | 0.370 | 0.356 |

| 1965+ | 41 | -3.729 | -0.088 | -0.460 | 0.858 | 0.554 | 0.290 |

| 1976+ | 30 | -15.225 | -0.765 | -3.034 | -0.527 | -0.348 | 0.636 |

Compared to WG’s reported d/p numbers:

| Spec | Ours | WG | Gap | |

|---|---|---|---|---|

| 1892+ | 114 | -2.06 | -2.06 | 0.00 |

| 1965+ | 41 | -3.73 | -3.69 | 0.04 |

| 1976+ | 30 | -15.22 | -15.14 | 0.09 |

The WG figures come from p. 1474 of the published paper (in-text table for 1892+ and 1976+) and from Table 1 column “Forecasts begin 1965” (1965+).

The longest window matches WG exactly to two

decimals. The two shorter windows are within 0.1 percentage

points. The pattern of the residual gap (zero on the long sample, small

on the short samples that are entirely post-1965) is consistent with

minor revisions to Goyal’s annual data file between the 2007 vintage

that fed the published paper and the version currently distributed on

Goyal’s website. The longest window draws most of its weight from

pre-1965 data that has not been revised. The shorter windows are

entirely post-1965 and show small drift in proportion to how

concentrated they are. Other plausible reconstructions (WG’s

log(1 + R - Rfree) plotting-script formula, hybrid

Shiller/CRSP returns, alternative OOS-start boundaries) do not close the

gap.

The deterioration of DP through time is unmistakable: a small negative in the long sample, more negative in 1965+, and substantially negative for 1976-2005. The McCracken (2004) and Clark-McCracken (2001) asymptotic 5% critical values for extra regressor are:

| π = P/R | MSE-F (5%) | ENC-NEW (5%) |

|---|---|---|

| 0.6 | 1.62 | 2.37 |

| 1.0 | 1.71 | 2.52 |

| 2.0 | 1.82 | 2.70 |

For the 1892+ window () MSE-F is small and ENC-NEW is below the 5% threshold. For the recent 30 years both statistics are firmly negative or near zero. No window supports a “DP beats the mean” conclusion under WG’s tests.

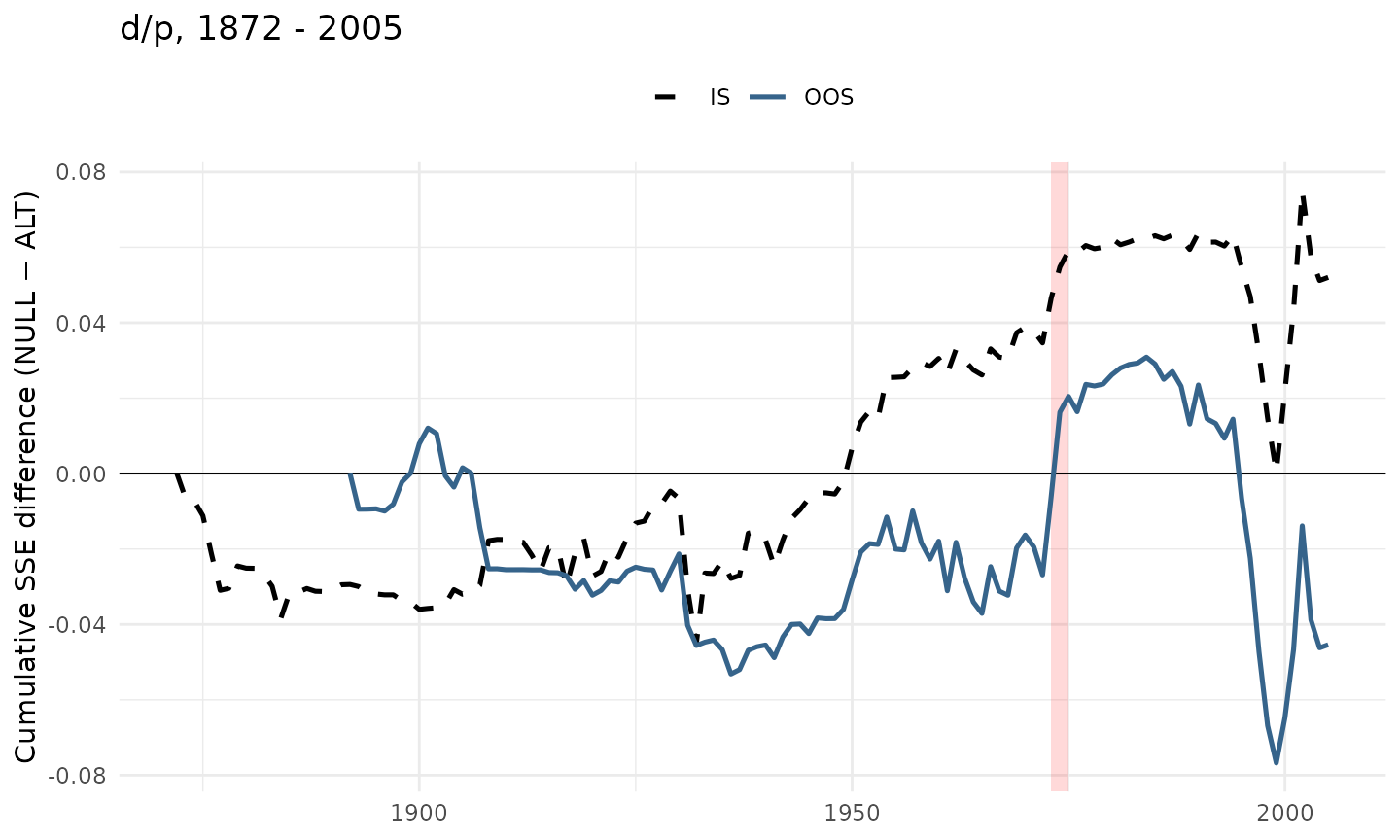

WG Figure 1: cumulative SSE difference for DP

WG’s signature visual is the cumulative squared-error difference

A rising line means the ALTERNATIVE beats the NULL up to that date, a falling line the opposite. The plot below mirrors the d/p panel of WG Figure 1 (IS = dotted, OOS = solid; Oil Shock 1973-1975 shaded in red).

# IS residuals from a single regression on the entire sample

fit_full <- lm(logeqp ~ log_dp_lag, data = wg)

is_xy <- residuals(fit_full)

is_mean <- wg$logeqp - mean(wg$logeqp)

# OOS residuals starting at year 21

R <- 20L

fc <- recursive_forecasts(wg$logeqp, wg$log_dp_lag, R = R)

is_imp <- cumsum(is_mean^2) - cumsum(is_xy^2)

oos_imp <- c(rep(NA, R), cumsum(fc$e_N^2) - cumsum(fc$e_A^2))

df <- data.frame(year = wg$year, IS = is_imp, OOS = oos_imp)

df_long <- rbind(

data.frame(year = df$year, kind = "IS", value = df$IS),

data.frame(year = df$year, kind = "OOS", value = df$OOS)

)

ggplot(df_long, aes(x = year, y = value, color = kind,

linetype = kind)) +

annotate("rect",

xmin = 1973, xmax = 1975,

ymin = -Inf, ymax = Inf,

fill = "red", alpha = 0.15) +

geom_hline(yintercept = 0, linewidth = 0.3) +

geom_line(linewidth = 0.9, na.rm = TRUE) +

scale_color_manual(values = c(IS = "black", OOS = "steelblue4")) +

scale_linetype_manual(values = c(IS = "dashed", OOS = "solid")) +

labs(x = NULL,

y = "Cumulative SSE difference (NULL − ALT)",

title = sprintf("d/p, 1872 - %d", max(wg$year))) +

theme_minimal() +

theme(legend.title = element_blank(),

legend.position = "top")

The replicated picture matches the d/p panel of WG Figure 1: a quiet first half-century, a climb from WW II to the early 1970s where DP modestly beats the historical mean, a peak around the Oil Shock, and a steep decline through the 1990s as the dividend yield collapsed during the dot-com bull market. The IS line (dashed) sits steadily above zero, so DP looks like a useful in-sample predictor. The OOS line (solid) eventually crashes through zero in the late 1990s. This gap between IS and OOS is what motivated WG’s “comprehensive look”.

Takeaway

For the dividend-price ratio at annual frequency, applied with WG’s own data and procedure:

- Long sample (1892+): every OOS statistic agrees that DP does not significantly beat the historical mean; the encompassing evidence is weak.

- 1965+ window: both and MSE-F turn clearly negative.

- Recent 30 years (1976+): the DP-augmented forecast is decisively worse than the historical mean.

This is the central message of Welch and Goyal about the dividend-price ratio: in-sample significance does not survive an honest out-of-sample evaluation, and the cumulative-SSE plot makes the structural break around the Oil Shock and the late-1990s decline immediate.

References

- Clark, T. E. and McCracken, M. W. (2001). Tests of equal forecast accuracy and encompassing for nested models. Journal of Econometrics, 105(1), 85-110.

- Clark, T. E. and West, K. D. (2007). Approximately normal tests for equal predictive accuracy in nested models. Journal of Econometrics, 138(1), 291-311.

- McCracken, M. W. (2007). Asymptotics for out of sample tests of Granger causality. Journal of Econometrics, 140(2), 719-752.

- Welch, I. and Goyal, A. (2008). A comprehensive look at the empirical performance of equity premium prediction. Review of Financial Studies, 21(4), 1455-1508.