This article replicates the out-of-sample Diebold-Mariano

panel of Table 1 in Rossi (2006), “Are exchange rates

really random walks? Some evidence robust to parameter instability”

(Macroeconomic Dynamics, 10(1), 20-38), using

dm_test() from forecastdom and the bundled

rossi2006 dataset.

The exercise is the classical Meese-Rogoff (1983) question: at the monthly horizon, can a small linear AR model of exchange-rate returns beat a driftless random walk out of sample?

library(forecastdom)

library(ggplot2)

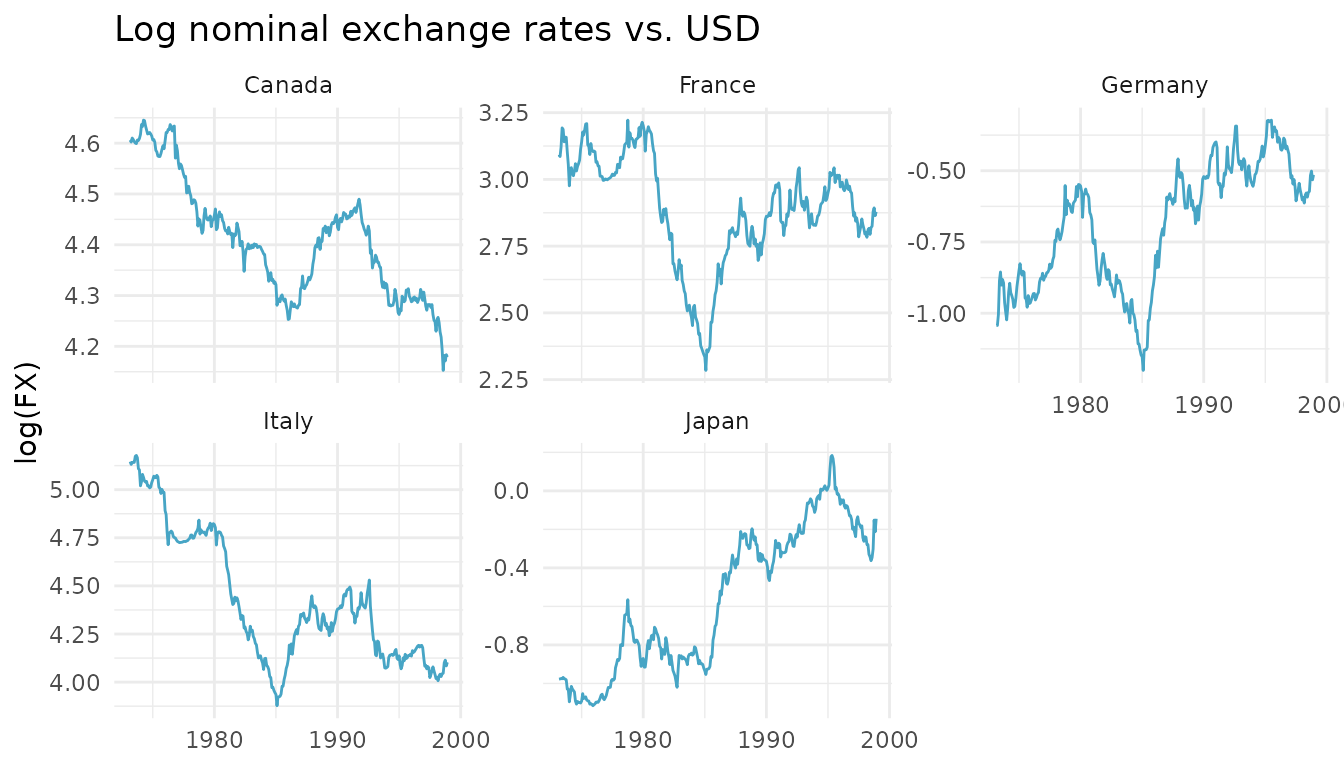

data(rossi2006)The data

Five bilateral nominal exchange rates against the U.S. dollar (Canada, France, Germany, Italy, Japan), monthly from March 1973 to December 1998, 310 observations per country.

ggplot(rossi2006, aes(date, log(fx))) +

geom_line(colour = "#47A5C5") +

facet_wrap(~ country, scales = "free_y") +

labs(x = NULL, y = "log(FX)",

title = "Log nominal exchange rates vs. USD") +

theme_minimal()

Forecasting setup

Let denote the log exchange rate and its monthly return. We compare two one-step-ahead forecasts of :

- Benchmark (driftless random walk): .

- Alternative (AR()): , with coefficients re-estimated each period.

Following Rossi, AR(1) and AR(2) share the same usable sample of returns. The first observations fit the initial model, and the remaining are evaluated out of sample. Three estimation schemes are considered:

- Split: coefficients estimated once on and held fixed.

- Recursive: coefficients re-estimated each period using all available data.

- Rolling: coefficients re-estimated each period using the most recent observations.

forecast_oos <- function(log_fx, p, scheme = c("split", "recursive", "rolling")) {

scheme <- match.arg(scheme)

T_full <- length(log_fx)

dy <- diff(log_fx)

Y <- dy[3:(T_full - 1)]

L1 <- dy[2:(T_full - 2)]

L2 <- dy[1:(T_full - 3)]

Xm <- if (p == 1) matrix(L1, ncol = 1) else cbind(L1, L2)

n_obs <- length(Y)

R <- as.integer(ceiling(n_obs / 2))

P_oos <- n_obs - R

e_alt <- numeric(P_oos)

e_bench <- numeric(P_oos)

for (j in seq_len(P_oos)) {

idx <- switch(scheme,

split = seq_len(R),

recursive = seq_len(R + j - 1),

rolling = j:(R + j - 1)

)

Z <- cbind(1, Xm[idx, , drop = FALSE])

b <- as.numeric(solve(crossprod(Z), crossprod(Z, Y[idx])))

pred <- as.numeric(c(1, Xm[R + j, ]) %*% b)

e_alt[j] <- Y[R + j] - pred

e_bench[j] <- Y[R + j]

}

list(e_bench = e_bench, e_alt = e_alt, P = P_oos)

}Replicating the OOS DM panel of Table 1

We call dm_test() with correction = FALSE

to match Rossi’s asymptotic

reference distribution. Rossi defines the loss differential as

,

so a positive DM statistic means the random walk has the lower

MSFE. To reproduce her sign convention we pass the AR errors as

e1 and the random-walk errors as e2.

countries <- levels(rossi2006$country)

schemes <- c("split", "recursive", "rolling")

run_panel <- function(p) {

out <- expand.grid(country = countries, scheme = schemes,

stringsAsFactors = FALSE)

out$DM <- NA_real_

out$DM_p <- NA_real_

for (i in seq_len(nrow(out))) {

log_fx <- log(subset(rossi2006, country == out$country[i])$fx)

fc <- forecast_oos(log_fx, p = p, scheme = out$scheme[i])

res <- dm_test(fc$e_alt, fc$e_bench,

alternative = "two.sided", correction = FALSE)

out$DM[i] <- res$statistic

out$DM_p[i] <- res$pvalue

}

out$cell <- sprintf("%.2f (%.2f)", out$DM, out$DM_p)

wide <- reshape(out[, c("country", "scheme", "cell")],

idvar = "scheme", timevar = "country", direction = "wide")

names(wide) <- gsub("^cell\\.", "", names(wide))

wide

}AR(1)

knitr::kable(run_panel(1), row.names = FALSE,

caption = "$DM_T$ statistic ($p$-value), AR(1) vs. RW")| scheme | Canada | France | Germany | Italy | Japan |

|---|---|---|---|---|---|

| split | 0.87 (0.38) | 1.38 (0.17) | -0.89 (0.38) | 0.80 (0.42) | -0.53 (0.60) |

| recursive | 1.16 (0.25) | 2.24 (0.03) | 0.14 (0.89) | 0.77 (0.44) | 0.00 (1.00) |

| rolling | 2.15 (0.03) | 1.77 (0.08) | 0.93 (0.35) | 0.60 (0.55) | 0.39 (0.69) |

AR(2)

knitr::kable(run_panel(2), row.names = FALSE,

caption = "$DM_T$ statistic ($p$-value), AR(2) vs. RW")| scheme | Canada | France | Germany | Italy | Japan |

|---|---|---|---|---|---|

| split | 1.97 (0.05) | 1.91 (0.06) | -0.03 (0.98) | 0.72 (0.47) | -0.64 (0.52) |

| recursive | 1.94 (0.05) | 1.71 (0.09) | 0.37 (0.71) | 0.73 (0.47) | 0.04 (0.97) |

| rolling | 2.29 (0.02) | 1.74 (0.08) | 0.79 (0.43) | 0.75 (0.45) | 0.41 (0.68) |

These cells reproduce the OOS DM panel of Rossi (2006) Table 1 exactly. The statistics are typically positive (the random walk has the lower MSFE), and the two-sided -values rarely fall below 5%. This is the classical Meese-Rogoff finding.

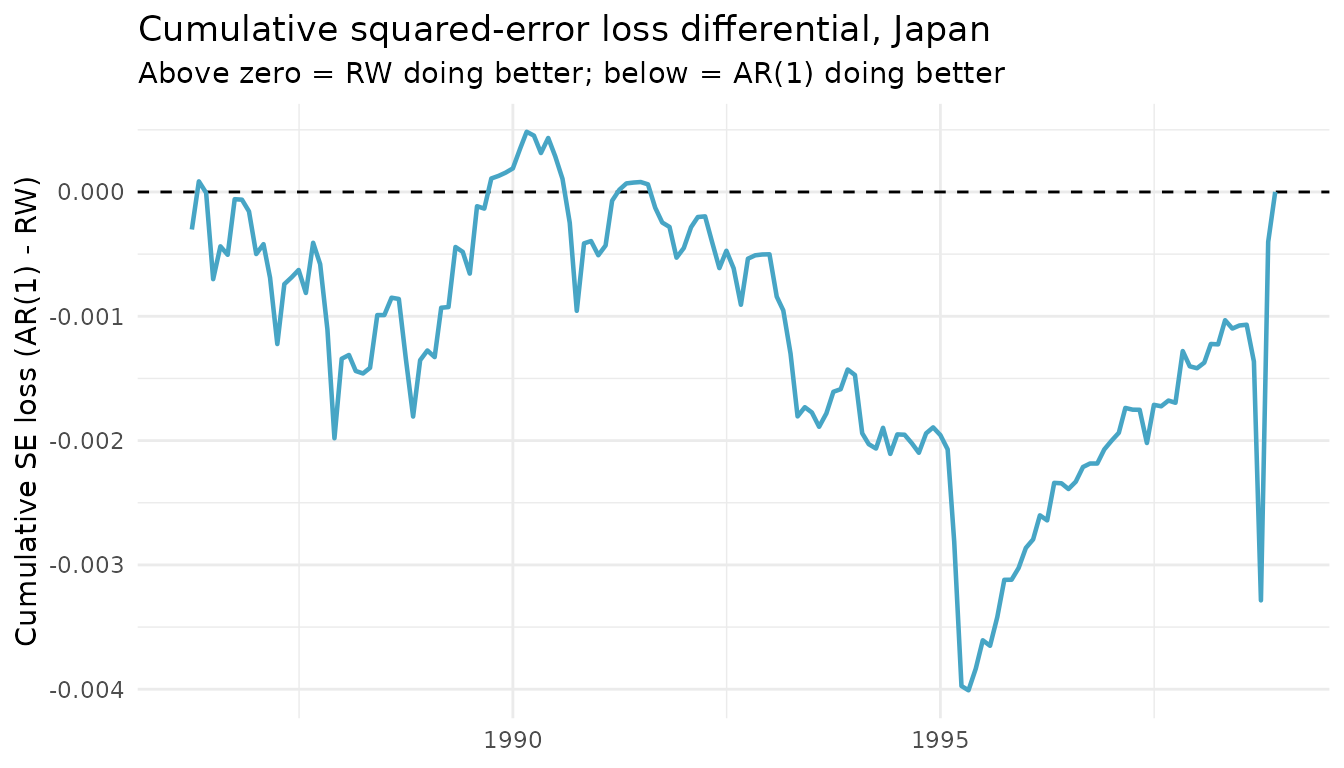

Single-country deep dive: Japan, AR(1), recursive

log_fx_jp <- log(subset(rossi2006, country == "Japan")$fx)

fc_jp <- forecast_oos(log_fx_jp, p = 1, scheme = "recursive")

dm_test(fc_jp$e_alt, fc_jp$e_bench, alternative = "two.sided", correction = FALSE)

#>

#> ╭────────────────────────────────────────────────────╮

#> │ Diebold-Mariano Test (1995) │

#> ├────────────────────────────────────────────────────┤

#> │ H0: Equal predictive ability │

#> │ H1: Methods have different predictive ability │

#> ├┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┤

#> │ Test Results: │

#> │ DM statistic: 0.0001 │

#> │ P-value: 0.9999 │

#> ├┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┄┤

#> │ Details: │

#> │ Observations (n): 153 │

#> │ Forecast horizon (h): 1 │

#> │ Loss function: SE │

#> │ Reference distribution: N(0,1) │

#> ╰────────────────────────────────────────────────────╯The cumulative squared-error differential, using Rossi’s sign convention so that positive values mean the random walk is winning, shows that the AR’s edge is concentrated in narrow sub-samples rather than spread uniformly across the OOS period.

loss_diff <- fc_jp$e_alt^2 - fc_jp$e_bench^2

oos_dates <- tail(unique(rossi2006$date), fc_jp$P)

ggplot(data.frame(date = oos_dates, cum = cumsum(loss_diff)),

aes(date, cum)) +

geom_hline(yintercept = 0, linetype = "dashed") +

geom_line(colour = "#47A5C5", linewidth = 0.8) +

labs(x = NULL,

y = "Cumulative SE loss (AR(1) - RW)",

title = "Cumulative squared-error loss differential, Japan",

subtitle = "Above zero = RW doing better; below = AR(1) doing better") +

theme_minimal()

References

- Diebold, F. X. and Mariano, R. S. (1995). Comparing predictive accuracy. Journal of Business & Economic Statistics, 13(3), 253-263.

- Meese, R. A. and Rogoff, K. (1983). Empirical exchange rate models of the seventies: Do they fit out of sample? Journal of International Economics, 14(1-2), 3-24.

- Rossi, B. (2006). Are exchange rates really random walks? Some evidence robust to parameter instability. Macroeconomic Dynamics, 10(1), 20-38.